Coca Cola is being valued like a slow growing bond proxy, but recent results show it can still compound through a mix of pricing, premiumization, and portfolio breadth. In Q3 2025, organic revenue grew 6% with price and mix up 6% and global unit case volume up 1%. That combination is the core of the long term story: steady volume with reliable revenue per case growth.

The stock at $70 implies investors are paying roughly a market multiple for a business with unusually stable demand and a long runway in zero sugar, hydration, sports, coffee, and tea. The DCF base case points to value above the current price, but the work product needs to be framed as a range, not a single point.

Target Change

| Rating | HOLD |

| Price (19 December 2025) | $70.06 |

| Price Target | % To PT | $101 | ↑44.16% |

| Market Cap | $ 292 B |

| Ticker | KO |

Business and operating momentum

Demand and pricing

- Q3 2025 net revenues grew 5% and organic revenues grew 6%.

- Price and mix grew 6%.

- Global unit case volume grew 1%.

- Coca Cola Zero Sugar grew 14% (clear proof that the portfolio is already shifting toward lower calorie options).

Cash generation

- Management guided to free cash flow excluding the fairlife contingent consideration payment of at least $9.8B for FY 2025 (built from about $12.0B cash flow from operations less about $2.2B capex).

Geography

- In Q3 2025: reported net revenue growth was strongest in Asia Pacific (11%) and EMEA (10%), with North America up 4% and Latin America down 4%.

This matters because it shows the model still works globally, but FX and regional macro can swing reported results.

Financial profile

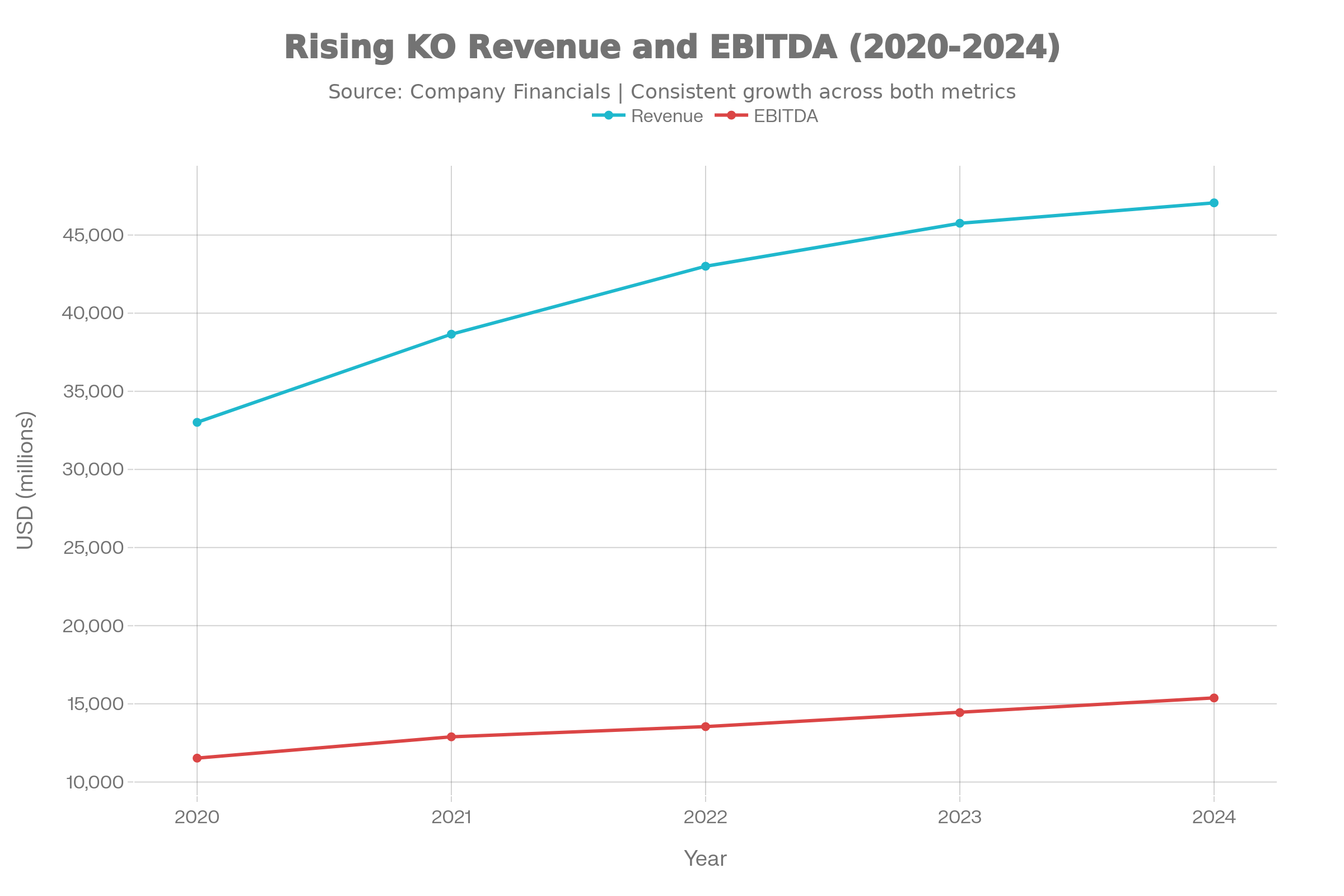

- Revenue: $47.1B in 2024 and $47.7B LTM Sep 2025.

- EBITDA: $15.4B in 2024 and $16.3B LTM Sep 2025.

- Unlevered free cash flow: $16.0B in 2024 (used as the base year for the DCF).

- Net debt: $32.38B (latest period).

- Shares outstanding: 4.302B (latest period).

KO revenue and EBITDA trend (2020 to 2024) shows steady expansion and supports the idea that mid single digit intrinsic growth is plausible even for a mature staple.

KO historical Revenue and EBITDA

Valuation framework

Intrinsic valuation (DCF)

The DCF is built off 2024 unlevered free cash flow of $15.997B.

Reason: 2025 LTM in the sheet looks distorted by one offs and working capital noise, while 2024 is a cleaner baseline for steady state earning power.

Key assumptions and the reasons behind them

1) Discount rate (WACC): 6.5%

- Defensive staples like KO usually merit a lower discount rate than the market.

2) Explicit free cash flow growth (Years 1 to 5): 4.5%

- KO guided to 5% to 6% organic revenue growth for FY 2025.

- Q3 2025 pricing and mix was 6% with volume positive, supporting the view that mid single digit growth can persist near term even if volume stays low.

- A 4.5% FCF growth rate is a small haircut to revenue guidance to reflect reinvestment, FX noise, and the reality that FCF does not always grow exactly with organic revenue.

3) Terminal growth: 2.5%

- A terminal growth rate should roughly track long run nominal GDP.

- For a global mature consumer staple, 2% to 3% is usually the reasonable band. 2.5% sits in the middle and avoids implying KO outgrows the economy forever.

Base case result (DCF): Implied fair value: $100.61 per share

Scenario Analysis

How the scenarios are defined:

- Bear case: higher WACC (rates and risk premium stay elevated), slower cash flow growth (health pressure plus weaker consumer), lower terminal growth. This is would happen when KO is still great, but macro and demand are worse than expected.”

- Base case: the assumptions described above.

- Bull case: lower WACC (rates normalize) and KO sustains stronger mix led growth (zero sugar, hydration, premiumization) without losing volume.

Trading comps

Quick implied price from peer multiples using KO LTM EBITDA ($16.307B), net debt ($32.38B), shares (4.302B):

| Multiple basis | EV EBITDA multiple | Implied price (approx) | Comment |

| PEP multiple | 13.10x | ~$42 | Low because PEP multiple is depressed by business mix and different growth profile |

| KDP multiple | 18.35x | ~$62 | Closer to KO, still below market |

| KO current multiple | 21.21x | ~$73 | Roughly matches the $70 stock price, so market is valuing KO near its own “normal” multiple |

| MNST multiple | 29.11x | ~$103 | Not realistic as a base case, but useful as an upside ceiling reference |

Comps explain why the market price can make sense even if the DCF looks cheap. The DCF upside requires believing KO will keep compounding cash flows near mid single digits and that the right discount rate is mid 6s, not mid 7s.

EV to EBITDA (TTM) multiples show how the market prices beverage peers:

- KO screens expensive versus PepsiCo on EV to EBITDA, but PepsiCo has a large snack business that changes its margin structure and growth drivers.

- Monster screens highest multiple because it has a very different growth profile.

- KO trading near 20x EV to EBITDA is broadly consistent with a defensive compounder positioning, not deep value.

Catalysts

- Q4 2025 earnings and 2026 guidance: expected Feb 10, 2026. This is where management can reset the narrative on volume, pricing, and cash flow.

- CEO transition: Henrique Braun becomes CEO effective March 31, 2026. These transitions often come with a refreshed capital allocation message, productivity targets, and portfolio priorities.

- Investor communications: KO investor relations currently lists no upcoming events, so earnings may be the next major formal update.

Key risks

1) GLP 1 and sugar exposure

- Circana estimates GLP 1 households are about 23% of US households and could represent 35% of food and beverage units sold by 2030.

- AlixPartners cites an average annualized impact of about negative 7% for soft drinks tied to GLP 1 behavior shifts.

Mitigant: KO is already driving large growth in zero sugar (14% in Q3) and expanding in water, sports, coffee, and tea.

2) FX and global macro

KO is global. Reported results can diverge from underlying trends when currency moves sharply. Q3 results explicitly highlighted currency headwinds and regional differences.

3) Valuation and rates

If the market requires a higher discount rate (7.5% plus), fair value can fall toward the current price fast.

Conclusion

KO looks attractive for a BUY if the goal is a high quality defensive compounder with real pricing power and portfolio breadth. The investment case is strongest under a steady growth, normalizing rates setup, where intrinsic value clusters above $70.